Key points

- From the 13 March 2026 trading day (14 March delivery), primary through tertiary① reserve products moved from weekly trading to day-ahead, 30-minute trading (source: Agency for Natural Resources and Energy / METI).

- Procured volume (required quantity) was cut from a 3σ basis to a 1σ basis; the 1σ-to-3σ band is now covered by the capacity market's reserve-utilization contract.

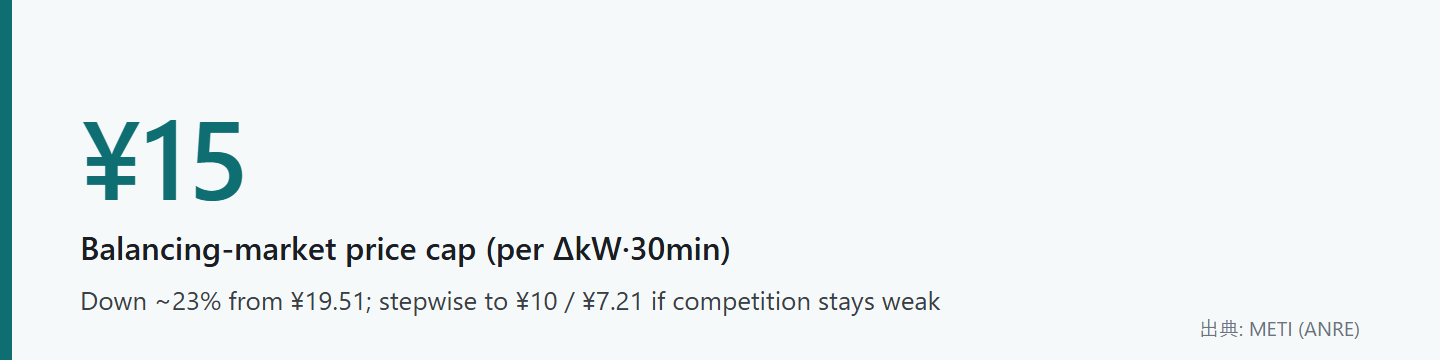

- The price cap was lowered from ¥19.51 to ¥15 per ΔkW·30min, with a stepwise path to ¥10 / ¥7.21 if competition does not improve. The EPRX trading fee doubled, from ¥0.03 to ¥0.06.

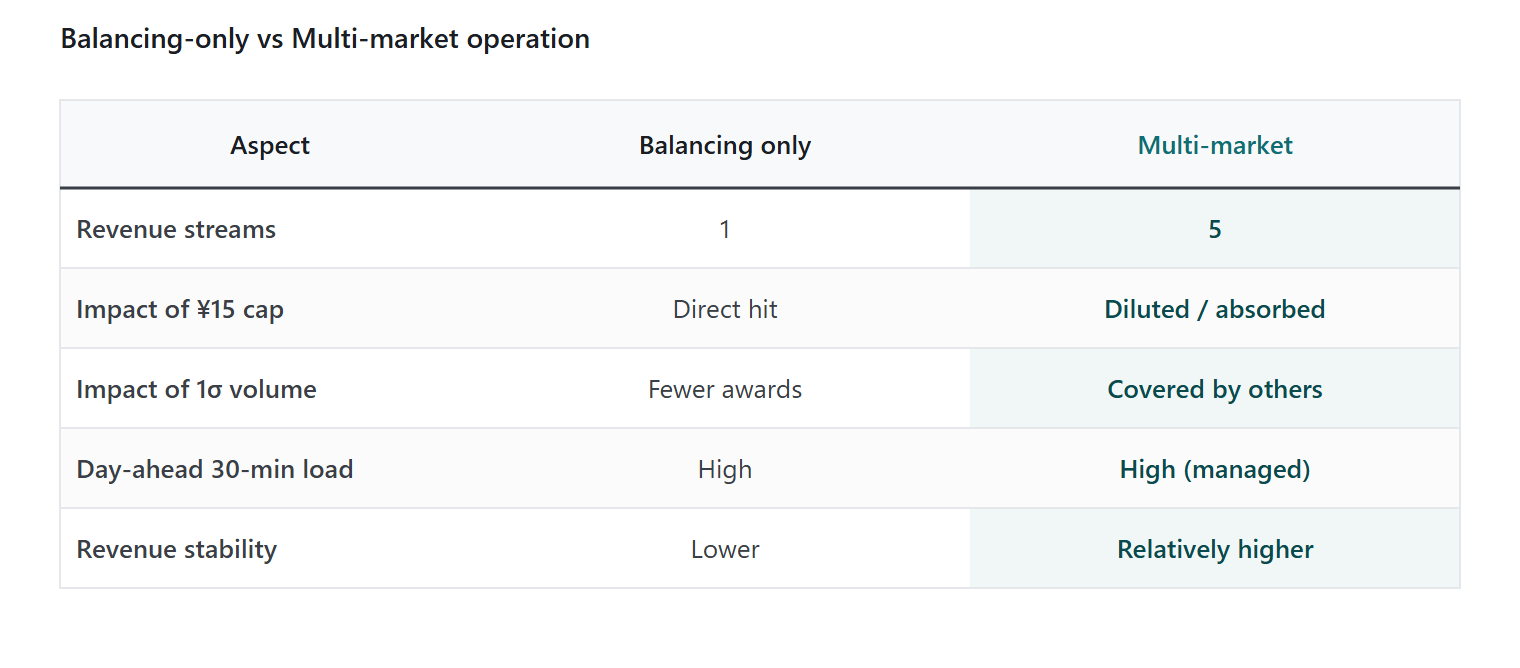

- A revenue model that depends on the balancing market alone now needs rethinking.

- The practical way to defend revenue is multi-market operation — combining Spot, intraday, capacity, and imbalance avoidance.

1. What Changed in the Balancing Market in March 2026

In short, the 13 March 2026 trading day (14 March delivery) is the dividing line: trading method, procured volume, price cap, and fees were all revised at once. From a battery operator's perspective, each pushes revenue down.

| Item | Before | From 13 March 2026 trading |

|---|---|---|

| Trading method | Mainly weekly trading | Day-ahead, 30-minute trading (primary–tertiary①) |

| Procured volume | 3σ basis | 1σ basis (1σ–3σ band via capacity-market reserve-utilization) |

| Price cap | ¥19.51/ΔkW·30min | ¥15 (stepwise ¥10 / ¥7.21 also specified) |

| Trading fee (EPRX) | ¥0.03/ΔkW·30min | ¥0.06 (doubled) |

Shift to day-ahead, 30-minute trading

Primary through tertiary① reserve, previously traded in weekly blocks, now trades the day before delivery in 30-minute slots. Bidding moves closer to delivery and prices vary slot by slot, so operators must make high-frequency bidding decisions the day before, factoring in demand, renewable output, and market-price outlooks.

Procured volume cut from 3σ to 1σ

The volume the market buys (required quantity) was reduced from a 3σ basis to a 1σ basis. Demand variation in the 1σ-to-3σ band is now handled not by market procurement but by the capacity market's reserve-utilization contract. For batteries, this means the total volume that can clear in the balancing market shrinks.

Lower price cap and doubled fee

The price cap for affected products fell from ¥19.51/ΔkW·30min to ¥15 — roughly a 23% cut on a unit-price basis.

※ Reduction: (19.51 − 15) ÷ 19.51 ≒ about 23% down. If competition does not improve, a stepwise reduction to ¥10 / ¥7.21 is specified in the rules.

In addition, the EPRX trading fee doubled, from ¥0.03 to ¥0.06 per ΔkW·30min. With the unit price falling while costs rise, margins are squeezed further.

2. Why Battery Revenue Gets Squeezed

The balancing-market payment to a battery centers on the payment for standby reserve capacity (ΔkW). This revision cuts directly into that.

※ ΔkW revenue ≒ price cap × bid kW × slots × operating days × award rate. If the cap falls, revenue drops by the unit-price difference even at the same award rate.

On top of this, the 1σ volume cut (fewer clearing opportunities) and the day-ahead 30-minute shift (higher forecasting difficulty) compound. Price down, volume down, harder to hit — these three pressures arrive together, so operators that relied on the balancing market as a single main revenue source are hit hardest.

3. Revenue Impact — the Risk of Single-Market Dependence

To be precise, the revision does not halve revenue uniformly. The magnitude depends on which products, at what utilization and award rate, an operator participated in. But the direction is clear: a revenue plan premised on the balancing market alone will overstate returns if it keeps using pre-revision figures.

For reference, the direction of impact in two scenarios (both indicative, not fixed values):

| View | Conservative | Central |

|---|---|---|

| Unit price | Prices in stepwise cuts (toward ¥10) | Assumes ¥15 holds for now |

| Cleared volume | Sharp drop in awards under 1σ | 1σ priced in, partly offset by capacity market |

| Revenue direction | Large downside if balancing-only | Downside partly absorbed via multi-market |

The key point is common to both scenarios: dependence on the balancing market alone has become riskier.

4. How to Defend Revenue — Multi-Market Operation

The practical countermeasure is to avoid depending on the balancing market alone and instead combine multiple markets (multi-market operation). A grid-scale battery has five main revenue sources.

- Spot (day-ahead) arbitrage — charge when cheap, discharge when expensive.

- Intraday market — capture price moves and forecast errors near delivery.

- Balancing market — price and volume shrank, but it remains a ΔkW revenue source.

- Capacity market (incl. reserve-utilization) — as the 1σ–3σ band shifted here, its relative weight rises.

- Imbalance avoidance — the value of containing settlement risk from supply-demand deviation.

Even if single-market (balancing-only) revenue is cut, stacking other markets can absorb part of the overall decline. After the revision, the operational skill of optimizing "how much to take in which market" slot by slot directly translates into a revenue difference.

5. The Practical Wall Owners Face — Why In-House Operation Is Hard

Multi-market operation is sound in theory, but it is heavy for a single battery owner to run alone. After the revision, the following loads fall on the owner.

- High-frequency bidding decisions are required the day before delivery, in 30-minute units.

- Spot, intraday, balancing, capacity, and imbalance must be watched together and allocated optimally per slot.

- Each charge/discharge is bound by state-of-charge (SOC) limits; committing to one market forfeits opportunities in another.

- Forecast accuracy for demand, renewable output, and market price directly drives revenue.

Running all of this for a single battery is demanding in both staffing and systems. Aggregation / operation outsourcing — bundling and operating multiple assets — is rational precisely because this simultaneous optimization can be handled by a dedicated team and system.

6. Principles for Honest Revenue Forecasting

The lesson of this revision is in how revenue forecasts are built. Just as procured volume shrank to 1σ and the excess shifted to the capacity market, the premise that "a given market pays stably" can move with rule changes. For investment decisions, the following principles apply.

- Do not premise a plan on a single market's high unit price and high award rate.

- Always present downside scenarios, such as the stepwise cap reduction to ¥10 / ¥7.21.

- Show a range with conservative and central scenarios; do not speak in a single point value.

In a downturn, honest revenue design framed as a range — not an optimistic point estimate — is what underpins the credibility of a project.

7. Where LehmanSoft Stands — Operation Outsourcing in the New Environment

LehmanSoft Japan is a Japan-based grid-scale battery aggregator and operator. We commercially operate our own 2.0MW/8.1MWh grid-scale storage station in Chichibu, Saitama, via AI-VPP, with trading on JEPX and participation in the balancing market. As an operator that runs assets ourselves, we understand the difficulty of — and the countermeasures for — multi-market operation in the new day-ahead, 30-minute environment from the practitioner's side.

Battery economics vary widely with capacity, grid area, market prices, eligibility, and SOC constraints. LehmanSoft provides operation optimization tied to market changes, centered on our grid-battery operation outsourcing service. A first-pass estimate for your own project can be run in our revenue simulator.

Conclusion

The March 2026 balancing-market revision squeezes battery revenue from three directions — price, volume, and fees. The keys to defending revenue in a downturn come down to three actions.

- Move your revenue premise from "balancing market alone" to "multi-market operation."

- Confirm a setup (in-house or outsourced) that can handle high-frequency, day-ahead, 30-minute operation.

- Re-estimate revenue in conservative and central scenarios, pricing in the stepwise cap reduction.

As a next step, run a first-pass estimate for your own project on the new basis in our revenue simulator. Related reading: How grid-battery revenue works in Japan: JEPX, capacity and balancing / Choosing an operation-outsourcing aggregator in Japan

References

- Agency for Natural Resources and Energy (METI), "On the Balancing Market" (13 May 2026) (https://www.meti.go.jp/shingikai/enecho/denryoku_gas/jisedai_kiban/stable_power_supply_wg/pdf/001_08_00.pdf)

- Organization for Cross-regional Coordination of Transmission Operators (OCCTO), "Status of the Balancing Market Review Subcommittee (FY2025 report)" (16 March 2026) (https://www.occto.or.jp/assets/chousei_117_04.pdf)

- Electric Power Reserve eXchange (EPRX), "Balancing Market Explanatory Material," 2nd ed. (13 March 2026) (https://www.eprx.or.jp/outline/docs/kaisetsu.pdf)

- OCCTO, "Capacity Market" (https://www.occto.or.jp/market-board/market/index.html)

This article is based on public information as of 9 June 2026. Rules, prices, and market design may change without notice; for actual investment decisions, consult the latest primary sources and a qualified advisor.